In light of the August RBA’s Statement on Monetary Policy, several key points stood out that could have an impact on the Australian property market. Scott O'Dell, Opteon's General Manager, Growth & Business Excellence, shares his observations and insights below.

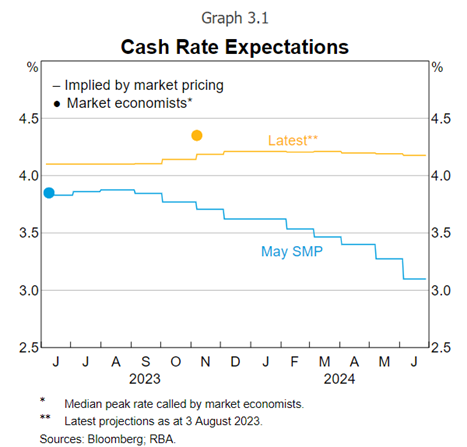

Cash rate expectations

The landscape for the cash rate has shifted since the prior statement in May.

Initially, there were discussions suggesting a peak and even impending potential cuts in the cash rate to alleviate the concerns surrounding mortgage stress, especially as borrowers transition off fixed rate loans.

However, the current sentiment amongst market economists suggests that the cash rate is expected to stay at its present level or perhaps experience a marginal increase till mid-2024.

This change in stance might have implications on real estate prices and the broader property market.

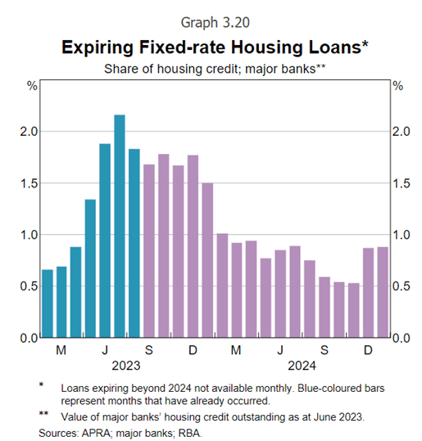

Fixed-rate loans and the 'Mortgage Cliff'

We are at an interesting juncture regarding fixed-rate loans. A considerable proportion of these loans will reach their expiration by the end of 2023.

Whilst we've already navigated through half of this 'mortgage cliff', it's estimated that about 10% of total housing credit is still on the horizon to transition off fixed rates.

This implies continued refinance activity with some tapering during the rest of 2023 and then back to more normal conditions through 2024.

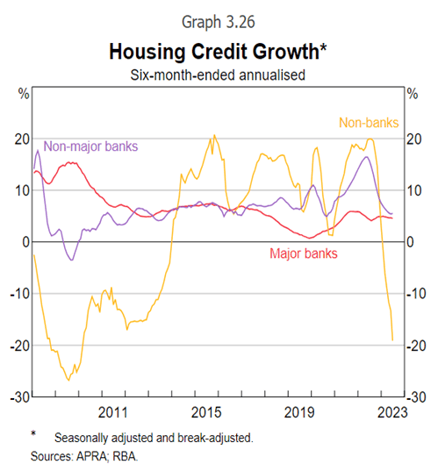

Lenders and their competitive stance

The RBA noted a reduction in competition between lenders has emerged over recent months. Home loan discounts have become scarcer, and many lenders have pulled back on cashback offers for both new and refinance borrowers.

This pullback may potentially affect valuation volumes in the short to medium term. It's worth noting that despite this, commitments for external refinancing remain relatively high, bolstered by borrowers transitioning from fixed-rate loans.

The graph shows a discernible drop in non-bank lending over the last 6 months which is not uncommon in periods of uncertainty. Non-Major banks have also recorded a sharp drop in lending growth recently after a period of clearly outperforming major banks.

In summary, the RBA's recent observations and forecasts provide us with valuable insights into the evolving Australian property landscape.

As property valuers, staying informed and understanding these shifts is vital in making informed decisions and providing top-notch advisory services to our clientele.

-1.png)