By Chris Mitrothanasis, Regional Director - Commercial & Agribusiness

The Australian Financial Review’s Property Editor, Nick Lenaghan, recently wrote that the alternative real estate market is “heavily under-represented in Australia’s listed property sector, a shortfall drawing increasing interest from major investors”.

Opteon data suggests that it is not just the institutional investors showing interest.

Buoyed by low interest rates and attracted by a range of factors, including compressing yields, individual and private investors are increasingly turning their attention to alternative real estate assets – particularly in the petroleum and childcare asset categories.

Why the interest?

In the past year, <$10m commercial, industrial and retail assets have remained fairly stable in a positive market across metro and regional locations. While these asset classes remain attractive to investors, many are also being drawn to alternative real estate assets as they can offer:

- better short-term returns – yields for this asset class are typically stronger in the short-term than for the more traditional property asset classes, particularly residential (which has historically attracted many individual and private investors)

- firming yields – boosted by increasing rents, particularly in NSW, and increases in capital value

- good income while awaiting redevelopment opportunities – sustained demand for large land sites, particularly in metro areas in Sydney and Melbourne, mean these assets can present good redevelopment opportunities

- strong capital growth – transaction prices across the vertical asset class have risen, particularly in Sydney and Melbourne

- robust, landlord-friendly lease terms – typically these include blanket recovery of landlord expenses, and

- weighted average lease expiries regularly exceeding 10-15 years – indicating very stable tenant bases and the use of lease covenants.

Beyond the attraction of investor benefits, we have seen demand for valuation of these assets also boosted by low interest rates, changed lending policies, refinancing requirements and strong marketing activities.

Vertical asset class performance

Two asset categories are performing particularly well in the <$10m alternative real estate asset class – petroleum and childcare. These categories are providing investors with secure long leases, good returns, capital growth and redevelopment opportunities. Other areas of strong valuation activity are being seen in motels, hotels, storage facilities and caravan parks.

One of the reasons petroleum and childcare assets are being embraced by individual and private investors is the active marketing they have received over the past five years. Stock levels are also being boosted by corporate owners, such as g8education, Caltex, Ampol and 7 Eleven, which are diversifying their portfolios. Many of these alternative real estate assets are sold with leaseback arrangements, making them more attractive to investors.

Overall, yields have compressed across regional and metro areas because of the low interest rate environment, an increase in investor demand and capital growth.

Petroleum assets

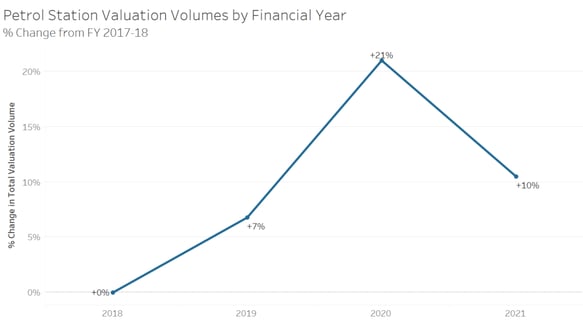

Over the past five years, Opteon has valued more than 600 petrol station sites in metro and regional areas (noting some properties were valued more than once). These have been in capital cities, key regional hubs and along main routes between cities. By volume, these properties were evenly split between being more traditional service stations (fuel and garage) and multi-purpose fuel outlets (fuel and convenience store).

Demand for these valuations has been increasing over the past four years, as shown in the graph below.

Larger petrol station sites have attracted many developers as they offer good holding income for potential redevelopment down the track. However, in most cases, petrol stations are being bought as lessor interests, many with current lease covenants and high WALE.

These lease covenants also inform due diligence on remediation risks, together with environmental assessments and site history investigations. This is particularly important for petrol station sites, as well as other sites, such as workshops, that have been used for petroleum storage.

Petrol stations have also seen an increase in retail sales as they evolved their convenience offerings. As these businesses continue to evolve, for example in the way Caltex has with Foodary, their attractiveness to lessors and lessees is likely to increase.

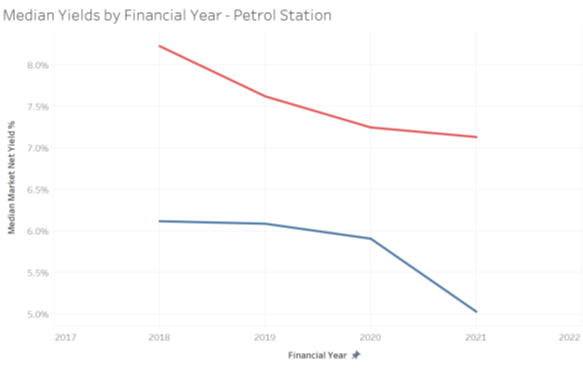

Over the past four years, market net yields on petrol stations have compressed in both metro and regional areas nationally, as shown in the graph below. In the 2021 financial year, 50% of yields were between 4.3% and 6.1% in metro areas and 50% of yields in regional areas were between 6.3% and 9.2%.

This reflects increased demand from the investor market, increasing rent rates, increasing transaction prices and the low interest rate environment.

Childcare assets

Childcare assets are appealing to many individual and private investors. Most investments are made for the lessor interest and holding potential, however approximately 20% are sold for the freehold and going concern.

Leases for childcare centres are typically standardised, with long initial lease terms of up to 30 years (source) . Rents have increased over last five years, aided by an increase in childcare daily rates.

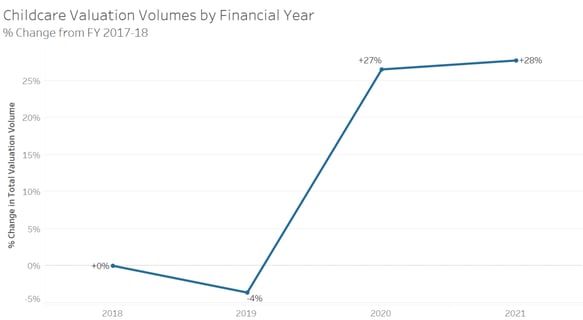

Opteon has conducted approximately 380 childcare property valuations over the past four years, with strong valuation activity in NSW (131 valuations), Victoria (76 valuations) and WA (74 valuations). These childcare centres have been located across the country and spread between metro (238 valuations) and regional (143 valuations) areas. By volume, these properties were evenly split between being day care centres and early childhood development centres (kindergarten and childcare).

Demand for these valuations has been increasing over the past four years, as shown in the graph below.

We have seen a notable increase in demand in regional areas during the past 18 months reflecting the pandemic-driven treechange trend embraced by many young families. This reflects increased demand from the investor market, increased government funding, increasing rent rates, increasing transaction prices and the low interest rate environment.

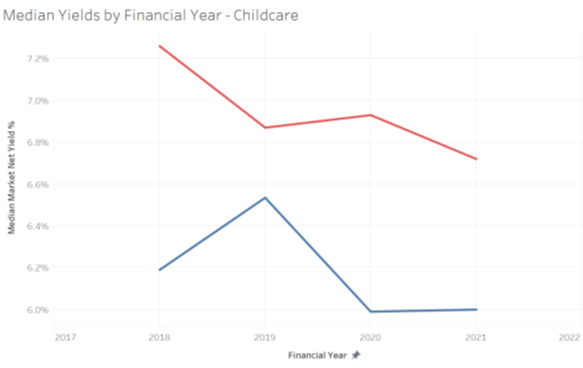

Market net yields on childcare centres have dropped in the last four financial years in regional areas across Australia and have dropped in the last three years in metro areas, as shown in the graph below. However, it is worth noting that, after strong compression (6.8% in FY 2018 to 5.4% in FY 2020) in recent years, there was a slight softening in the Sydney metro market for childcare centres, with median yields ranging from 5.4% – 5.7%.

In the 2021 financial year, 50% of yields were between 5.6% and 6.7% in metro areas and 50% of yields in regional areas were between 6.3% and 7.1%.

The COVID-19 impact

In very different ways, petrol stations and childcare centres are key to the country’s productivity. As such, the businesses associated with these alternative real estate assets have attracted both financial and essential worker status support from governments during the pandemic.

The childcare sector has attracted significant government funding and support during the pandemic, helping ensure the sector remains financially stable and open for business. This has allowed many essential workers to go to work and other employees to remain productive when working-from-home.

The pandemic has “pumped up” the service station asset class, with one market commentator noting: “With long leases to national tenants and greater exposure to domestic travel due to the pandemic, service stations remain well-placed to outperform all other asset classes (source).” Anecdotally, we have also seen rises in convenience sales during lockdowns.

DISCLAIMER

This material is produced by Opteon Property Group Pty Ltd. It is intended to provide general information in summary form on valuation related topics, current at the time of first publication. The contents do not constitute advice and should not be relied upon as such. Formal advice should be sought in particular matters. Opteon’s valuers are qualified, experienced and certified to provide market value valuations of your property. Opteon does not provide accounting, specialist tax or financial advice.

Liability limited by a scheme approved under Professional Standards Legislation.

.png)

.png)