By Ross Turner, National Director - Commercial Agri Advisory

Following sustained growth and value uplift, yields on residential flats and multi-residential property reached all-time lows during the pandemic. This led to a noticeable pivot by investors to commercial property. This shift in focus, along with low interest rates, has driven a healthy sales recovery in select national commercial markets – particularly the sub-$10 million owner occupied and investment space.

The second wave of lockdowns across Australia led to many sub-$10 million investors contemplating the fundamentals of the commercial property sector. In the post-pandemic onset, one of the most important factors quickly became the underlying ability of commercial tenants to sustain rental payments.

Addressing the risks of commercial leases

One of the largest points of difference between residential and commercial investment property is that commercial leases are negotiated for longer terms (usually 2-10 years). These leases typically have structured provisions that allow for the rent to increase annually over the term of the lease.

The COVID-19 lockdowns and restrictions highlighted the need for investors to confirm that the tenant can sustain rental payments and rental increases over the term of their lease. For investors, there are two risk factors to consider when assessing the sustainability of income for an asset:

-

the strength of the tenant covenant (i.e. the ability and financial strength of the tenant/lessee to pay rent), and

-

the rental growth provisions in the lease and how these co-relate with market growth within the tenant’s asset class.

Strength of tenant covenant

The strength of a leasing covenant is determined by the financial strength, credit profile and balance sheet capacity of the tenant to sustain rental payments. For example, government tenants are very attractive because the risk of rental payment default is all but eliminated due to the very low level of sovereign risk in Australia. Similarly, if corporate tenants are backed by a strong balance sheet, the tenant covenant is likely to be one that features income security that in turn will ensure the property keeps generating income.

As tenants, smaller businesses – especially those in industries that have been negatively affected by the pandemic – are often riskier. As sustainability of rental payments could be compromised, any balance sheet volatility warrants further due diligence and risk assessment if an impacted business comprises part of the tenancy mix of a property.

Rental growth provisions in the lease

One of the most important, but potentially least discussed, items in the sustainability of income in commercial property is the growth profile of the rent outlined by the provisions of the lease, and how this may differentiate from market leasing transactions at any point in time in the property cycle.

It is also important to note that leases negotiated before the onset of COVID-19 pandemic may not reflect the future growth projections in the new COVID normal economy.

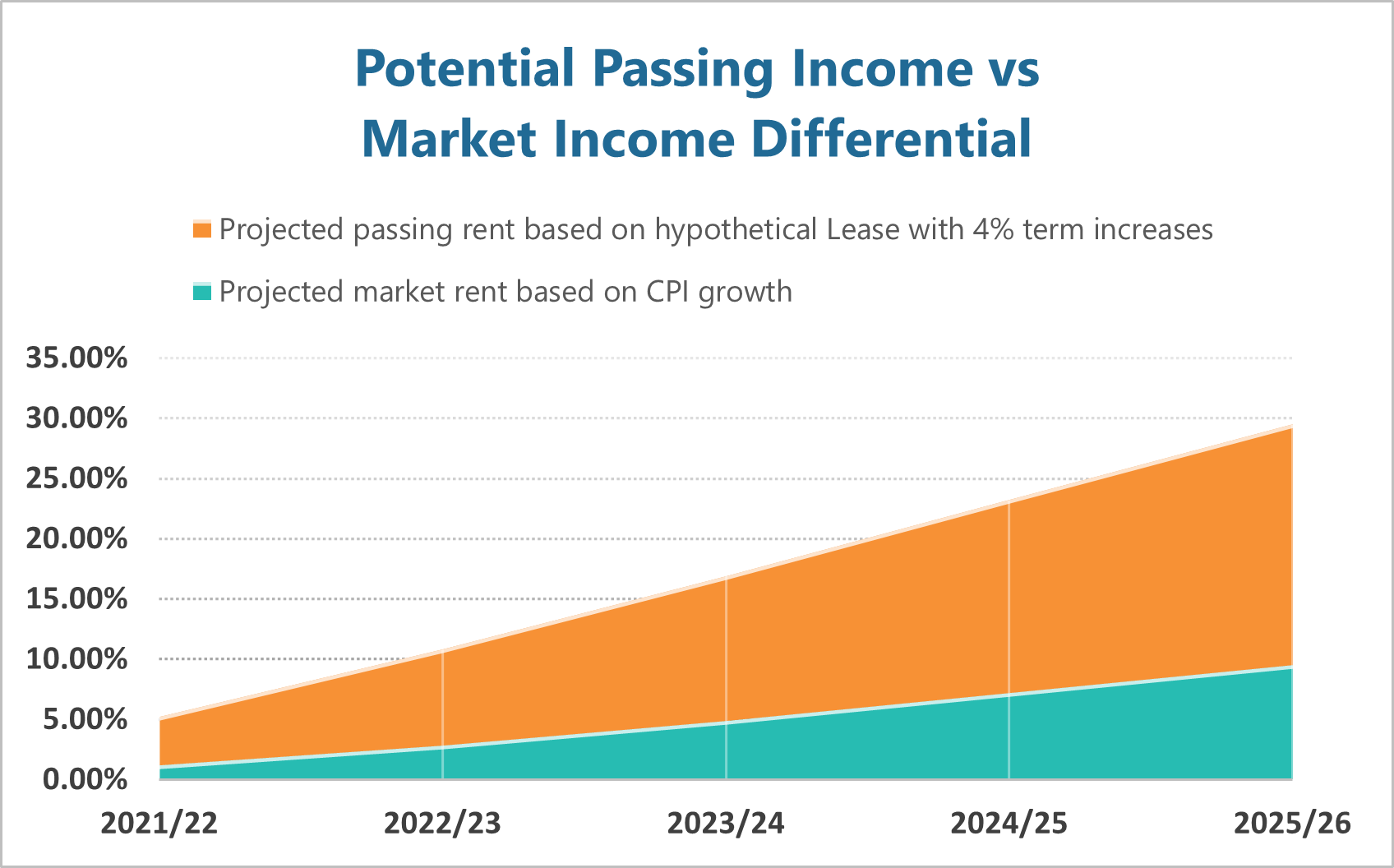

Before the pandemic, some commercial leases were structured with 3%-4% fixed rental increases over the term of the lease. In contrast, leases featuring growth rates based on CPI are not faring as well. Data from Deloitte Access Economics shows an average CPI growth forecast of 1.9% per annum for the next five years. Whilst inflation is currently a key topic of discussion, not all markets are created equal, and it should be noted that any potential inflationary pressures to rents would need to be balanced by demand levels changing from new work and consumer buying patterns post-pandemic.

Figure 1 shows the growing cumulative differential to a lease with a 4% contracted growth provision compared to one with projected CPI growth provisions. Using this example, this creates a significant gap of 10.5% between projected passing and market rent in 2025/26.

Figure 1: A significant income gap is created when moving from a 4% contracted growth provision to a CPI growth provision.

While rental growth has been impacted by COVID-19, particularly in industries such as retail and hospitality, it has not necessarily been priced into current market transactions. This is because rental growth is a lag metric that takes time to impact underlying property values. It can also be potentially hidden by other measures, such as tenant incentive side agreements.

Tenants will also be aware of this difference. Leases negotiated before the pandemic with fixed increases will need to be monitored closely to gauge their long-term sustainability. Using the graphed example, and assuming the growth of parts of the economy does not strengthen, there is the possibility that market rents will not align with passing rents at the end of a fixed lease term. That outcome will increase several risks, as outlined below.

Weighing the risks

When monitoring commercial portfolios or performing due diligence on a commercial property acquisition, it is important to understand, manage and mitigate the various risks to income. Three factors to consider are:

-

the diminishing probability that the tenant will renew the lease for a further term

-

the ability of the tenant to sustain rental payments during the period of the lease if they do not have the right financial capacity, and

-

the sustainability of the property’s value, as adjustments will need to be made if there is a noted differential between passing and market rent, with the added value of any profit rent diminishing towards the end of the lease term.

By doing so effectively, investors can help protect the sustainability of income and the value of their asset.

Tenant renewal

There are measures in a lease that can protect landlords from a sitting tenant’s rent falling below a previous years rent in the event of a lease renewal, including cap and collar provisions, and rachet clauses. However, it is worth considering whether there is a higher level of risk that the sitting tenant may not renew the lease on expiry. If that is the case, it may be worth provisioning for higher incentives, leasing costs and downtime.

Sustainability of rental payments

Similarly, landlords can be protected against non-payment of rent by provisions such as personal guarantees, security deposits and bank guarantees. However, if the passing/contract rent is above the level of rent indicated by market transactions that may flag a warning that the level of contract rental may not be sustainable for the tenant.

Depending on the strength of their business, this could increase the risk of tenant default. That scenario would be reflected in the risk profile of the asset and would impact the property’s valuation.

Sustainability of property value

Finally, as market net income is a fundamental value driver of commercial property, it is important to note that risks to the sustainability of income ultimately may impact the value of a property. This could be caused by the introduction of incentive provisions, downtime, leasing agents’ allowances, or the adopted net yield/capitalisation rate/discount rate softening to allow for the risks in the income profile.

Author

Author

Ross Turner

National Director - Commercial Agri Advisory

M: +61 435 039 847

![]()

DISCLAIMER

This material is produced by Opteon Property Group Pty Ltd. It is intended to provide general information in summary form on valuation related topics, current at the time of first publication. The contents do not constitute advice and should not be relied upon as such. Formal advice should be sought in particular matters. Opteon’s valuers are qualified, experienced and certified to provide market value valuations of your property. Opteon does not provide accounting, specialist tax, investment or financial advice.

Liability limited by a scheme approved under Professional Standards Legislation.

.svg)

.png)